One of the most common misconceptions among buyers? That their credit score isn’t good enough to get a home loan.

According to a Fannie Mae survey, 90% of buyers either overestimate the credit score required or don’t know it at all and that misunderstanding could be keeping you on the sidelines unnecessarily.

Let’s clear it up. You don’t need a perfect score to qualify for a mortgage. In fact, your options might be broader than you think.

There’s No One Magic Number

Despite what you may have heard, there isn’t one universal credit score you need to buy a home. Lenders look at a range of scores depending on the loan type and that opens doors for more people.

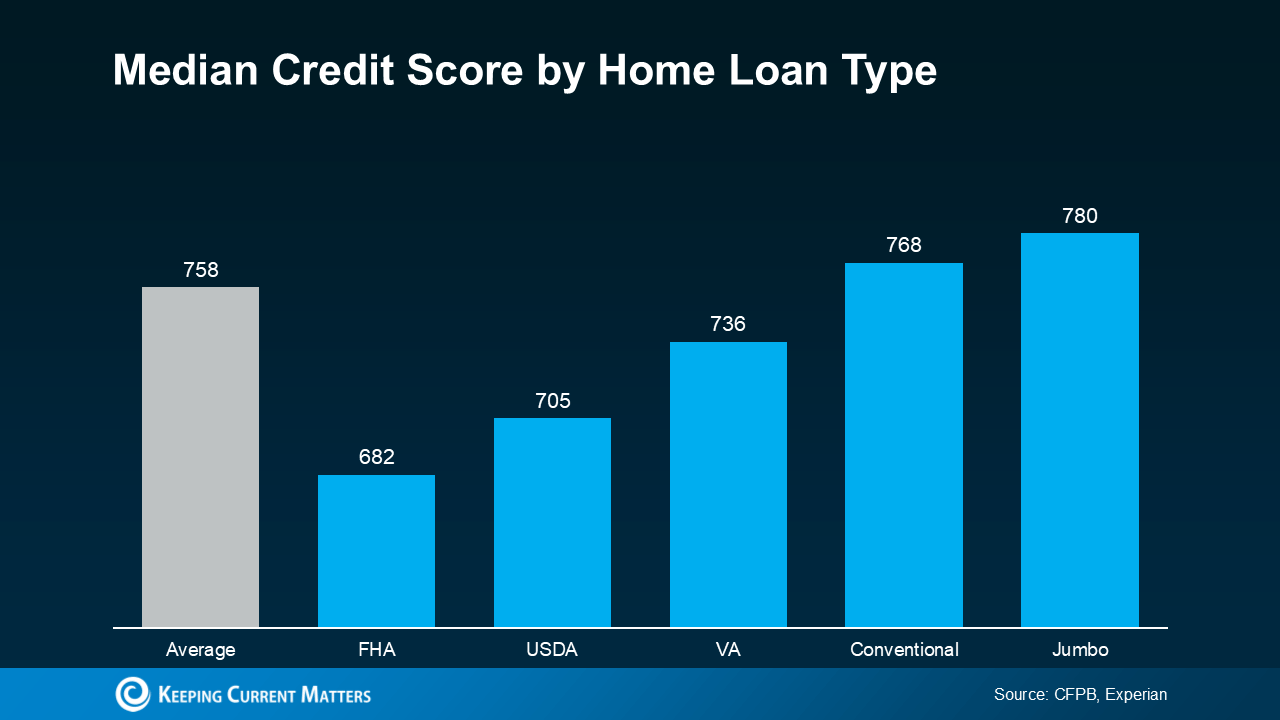

Here’s the median credit score by home loan type, based on recent data from Experian and the CFPB:

Photos credits: Keeping Current Matters

As you can see, government-backed loans like FHA and USDA are accessible even with scores in the 600s. VA loans (for eligible veterans and service members) also offer flexibility.

“While many lenders use credit scores like FICO Scores to help them make lending decisions, each lender has its own strategy... There is no single ‘cutoff score’ used by all lenders.” – FICO

Why Your Credit Score Still Matters

Even if you don’t need an elite score to qualify, your credit still plays a critical role in:

- What loan types you can access

- The interest rate you’ll get

- The terms and conditions of your mortgage

Higher scores usually mean lower rates which could save you tens of thousands over the life of your loan.

“Typically, the higher your score, the lower the interest rates and better terms you’ll qualify for.” – Bankrate

But don’t stress. You don’t need a perfect score. Plenty of buyers secure financing with average credit.

Want To Improve Your Score Before Buying?

Here are four smart strategies to help boost your credit before applying for a home loan, according to the Federal Reserve Board:

- Pay your bills on time – Late payments are one of the fastest ways to hurt your score.

- Reduce your credit card balances – Lower debt = better risk profile in a lender’s eyes.

- Check your credit report for errors – Fixing mistakes could give you a quick score bump.

- Avoid opening new accounts – Too many inquiries can temporarily lower your score.

Final Thoughts

Don’t assume you’re not qualified to buy a home because of your credit score. The truth is, there are flexible options out there and the best first step is connecting with a knowledgeable local lender who can walk you through your specific options.

If you’re not sure where to start, I can connect you with trusted lending professionals who’ll give you a realistic, no-pressure assessment.