The Federal Reserve (the Fed) meets this week, and expectations are high that they’ll cut the Federal Funds Rate but does that mean mortgage rates will automatically drop? Let’s clear up some common misconceptions and talk about what this could mean for you as a homeowner or buyer in today’s real estate market.

THE FED DOESN'T DIRECTLY SET MORTGAGE RATES

Right now, all eyes are on the Fed. Most economists expect they’ll cut the Federal Funds Rate at their mid-September 2025 meeting to head off a potential slowdown in the economy.

Photo copyright © 2025 Keeping Current Matters

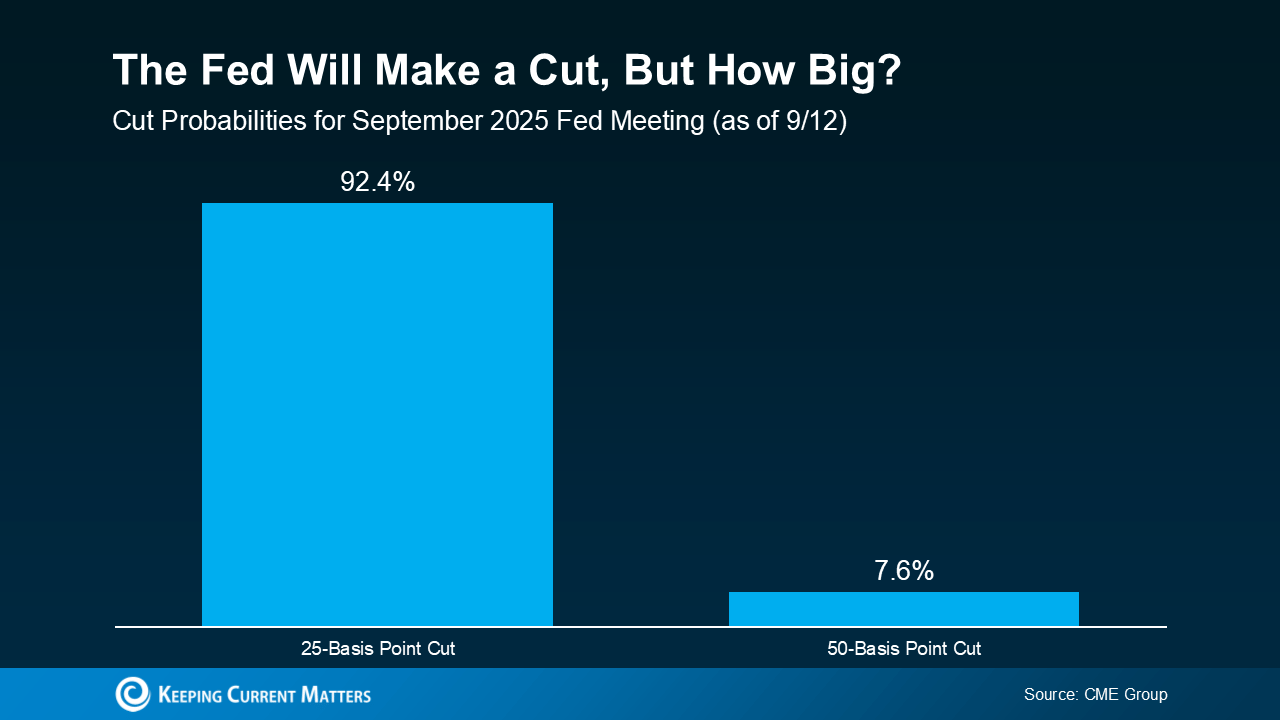

According to the CME FedWatch Tool, the odds are nearly locked in:

- 92.4% chance of a small 25-basis point cut

- 7.6% chance of a larger 50-basis point cut

So, what exactly is the Federal Funds Rate? It’s the short-term interest rate banks charge each other. It influences borrowing costs across the economy, but it’s not the same thing as mortgage rates. Still, the Fed’s moves often shape the direction mortgage rates take next.

WHY MARKETS ALREADY SAW THIS CUT COMING

Here’s the surprising part: mortgage rates usually respond to what financial markets expect the Fed will do, before the Fed even makes its announcement.

When weaker-than-expected jobs reports came out on August 1 and September 5, mortgage rates dipped. Why? Because markets became more confident the Fed would cut soon, and those expectations were priced in immediately.

That’s why if the Fed makes the widely expected 25-basis point cut, mortgage rates may not shift dramatically — that move is likely already baked in. But if the Fed surprises with a 50-basis point cut, mortgage rates could come down further in the short term.

WHERE DO MORTGAGE RATES GO FROM HERE?

One single cut won’t move the needle much. But here’s where it gets interesting:

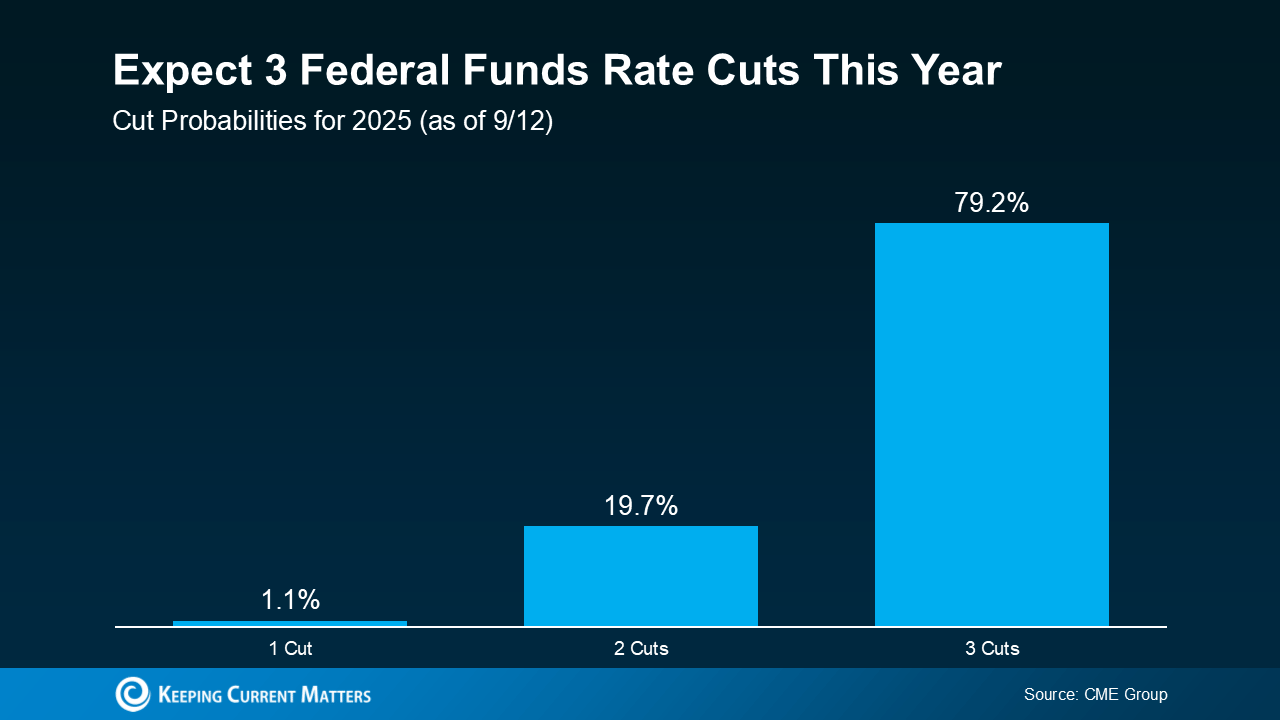

Markets currently expect the Fed could make up to three cuts before the end of 2025 (see chart below).

Photo copyright © 2025 Keeping Current Matters

As Sam Williamson, Senior Economist at First American, explains:

For mortgage rates, investor confidence in a forthcoming rate-cutting cycle could help push borrowing costs lower in the back half of 2025, offering some relief to housing affordability and potentially helping to boost buyer demand and overall market activity.

That means multiple cuts — or even the expectation of them — could help mortgage rates ease further heading into late 2025 and into 2026.

Of course, this all depends on how the economy evolves. A surprise inflation spike or stronger-than-expected growth could shift the Fed’s plans quickly.

FINAL TAKE AWAY

Mortgage rates won’t fall in lockstep with the Fed, and they likely won’t drop overnight. But if the Fed enters a true rate-cutting cycle, there’s a strong chance we’ll see more favorable mortgage rates later this year and into 2026.

If you’ve been waiting on the sidelines, now is the time to talk strategy. Even a small rate drop can make a meaningful difference in affordability — and in the competitive real estate market of Annapolis and the Chesapeake Bay region, timing is everything.

CONSIDERTING BUYING, SELLING, OR RENOVATING?

Whether you’re planning your next move or just want to protect your current investment, staying ahead of financial shifts like Fed rate cuts is key. LET'S CONNECT!

WEATHERTEK HOME EXTERIORS

If your home’s roof is on your mind, my company WeatherTek Home Exteriors is here to help.

From free drone inspections to transparent estimates, We make roof replacement and maintenance stress-free. Realtors and past clients even earn a 15% referral bonus.

📞 Call us today at 443-332-3035 to schedule your free inspection.