50-Year Mortgages: The Real Cost for Maryland Homebuyers (And Why I Think It’s a Terrible Idea)

Buying a home on the Chesapeake Bay already brings enough financial decisions, interest rates, down payments, inspections, insurance, and all the things that matter when you’re budgeting long-term. Now we’re hearing discussions again about the idea of a 50-year mortgage. On the surface, it sounds tempting: “Hey, lower monthly payments—sign me up!”

But once you dig in?

The numbers tell a very different story.

As a top-producing real estate agent in Annapolis who works daily with buyers, sellers, and investors, I want you to be fully informed, like you and I are having a real conversation over coffee. So let’s break this down in simple, human terms.

What Is a 50-Year Mortgage?

A 50-year mortgage stretches your payments over, yep, half a century. That means lower monthly payments, but you’re also renting money from the bank for an extra 20 years beyond a standard 30-year mortgage. And the interest? It balloons almost beyond imagination.

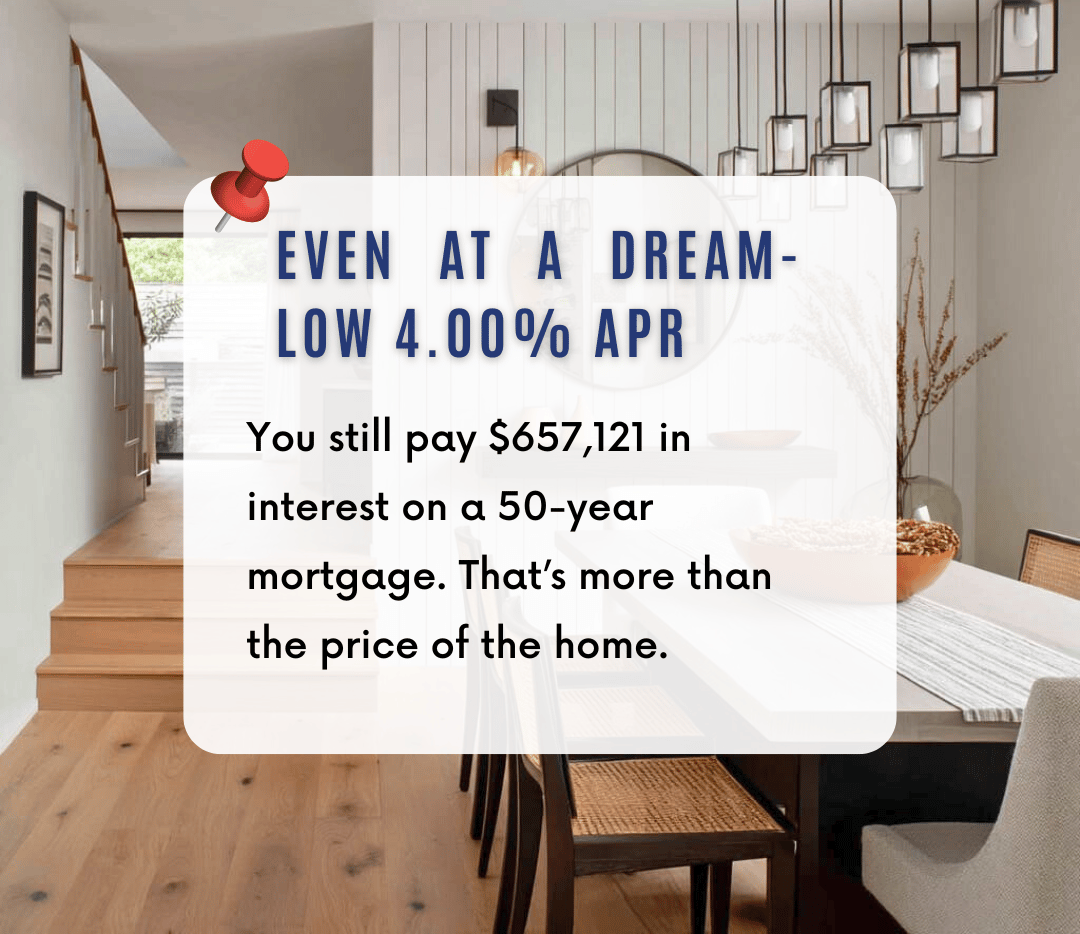

Even if rates stayed the same (which they won’t), the total amount you’d pay in interest would be staggeringly higher.

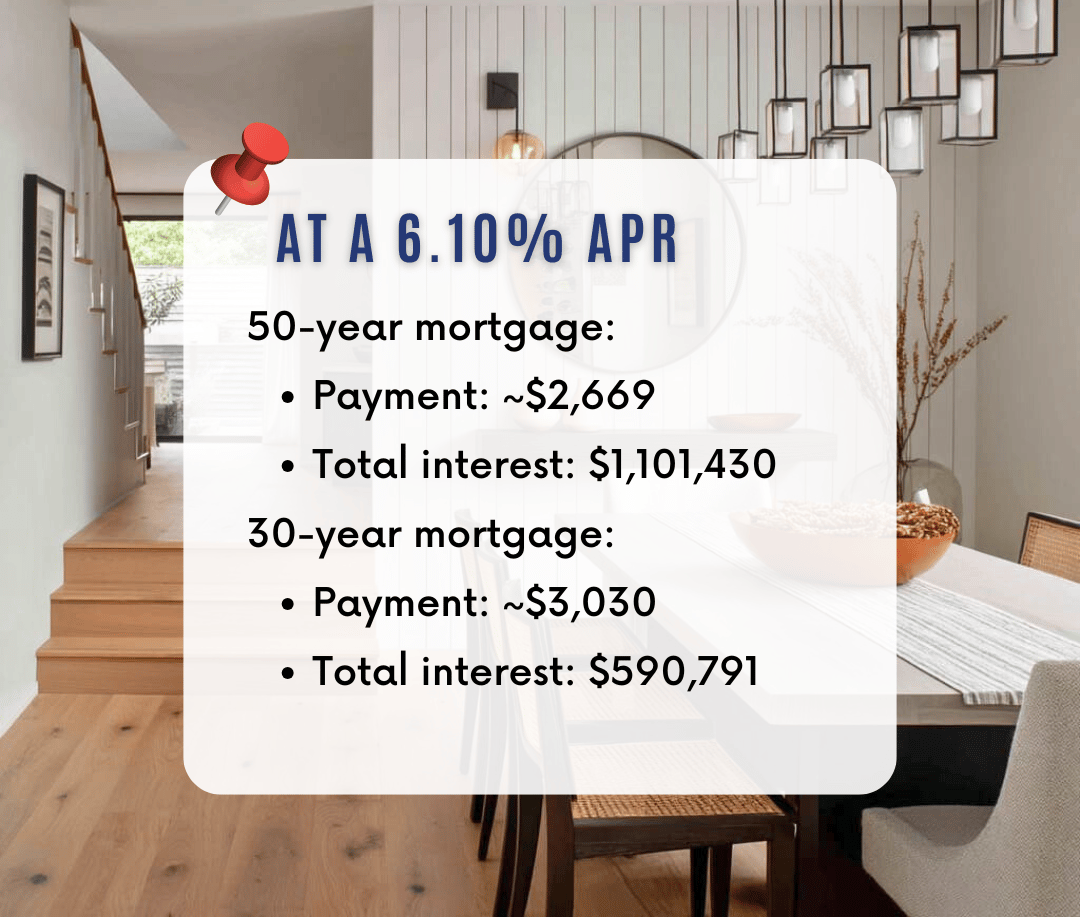

How Much More Would a 50-Year Mortgage Actually Cost?

Using the same $500,000 loan example referenced in the original financial analysis, here’s what it really looks like:

You’d pay nearly double in interest with a 50-year mortgage.

Again—almost double.

So while the monthly payment is lower each month, your long-term cost is… well, insane.

50-Year Mortgage = Extremely Slow Equity Growth

Equity is wealth. It’s how homeowners build net worth. With a 50-year mortgage, you barely chip away at the principal for decades.

- After 10 years on a 50-year mortgage: You’ve paid off: 4% of the original balance

- After 10 years on a 30-year mortgage: You’ve paid off: 16%

That’s a massive gap, and it directly affects your financial flexibility, selling options, HELOC availability, and long-term wealth-building.

In a shifting market (especially here in Annapolis and the Chesapeake Bay region), slow equity growth can put homeowners underwater far more easily.

Why This Matters for Annapolis, Chesapeake Bay & Maryland Buyers

Homes in our region—especially waterfront and water-privileged communities—tend to hold long-term value, but they also come with unique expenses:

- Flood insurance

- Dock maintenance

- Community fees

- Waterfront upkeep

- Higher utility costs

When you add a 50-year mortgage on top of that, it becomes harder to build wealth and easier to fall into long-term debt traps.

Better Ways to Lower Your Mortgage Costs Right Now

Instead of jumping into a half-century loan, here are smarter strategies:

- Shop around for lenders

- Consider buying down your rate

Temporary or permanent buydowns can make a real difference. - Improve credit before applying

Even a 20-point jump can reduce your rate.

(External reference: https://www.nerdwallet.com/article/mortgages/how-to-improve-your-credit-score) - Adjust price points or locations

There are fantastic waterfront-adjacent neighborhoods in Annapolis that offer better value while keeping you close to the Bay lifestyle. - Explore 15-year or 20-year mortgage alternatives

These build equity faster and dramatically reduce interest paid.

My Professional Opinion (And Personal Stance)

As someone who has helped hundreds of families buy and sell homes over 23+ years in Annapolis, I'll be blunt: I think a 50-year mortgage is a terrible idea.

Yes, it lowers the monthly payment. But it also:

- Drains wealth instead of building it

- Delays financial independence

- Increases risk during market downturns

- Leaves you paying double—or more—in interest

- Slows equity so much that selling becomes harder

- Penalizes responsible homeowners long-term

In my view?

If you need a 50-year mortgage to afford a home, the home might simply be overpriced for your current situation—or the mortgage product is predatory by design.

There are smarter, safer, wealth-building paths forward.

Key Takeaways

- A 50-year mortgage drastically increases total interest paid.

- Equity grows painfully slowly—bad for long-term wealth.

- Annapolis buyers face additional waterfront-related expenses that make long-term debt even riskier.

- There are far better ways to reduce monthly payment stress.

- My stance: 50-year mortgages are financially dangerous for most buyers.

Ready to Prep Your Home for Winter or Strategize Your Next Move?

Whether you're thinking about refinancing, buying, selling, or prepping your waterfront home for winter, I’m here to help you make the right financial decisions—not the ones that might trap you in decades of unnecessary debt.